by Phil Slinger – CAB Chief Executive

According to the ONS construction monthly construction output in February decreased by 0.1% to £14,610 million in volume terms compared to January. This is the first monthly decrease since October 2021. The Construction Industry output is likely to have been affected because of Storm Dudley, Eunice and Franklin, losing more days than usual over the period, but some other businesses will have picked up repair and maintenance work following the storms.

Despite the effects of the weather, material shortages continue to dog the industry coupled with higher costs which are particularly affecting the smaller businesses. Good news is that demand continues to be strong with construction orders increasing by 9.2% in the final quarter of 2021 compared to quarter three 2021.

It is not clear yet what the effects of the war in the Ukraine will have on UK Construction. The CAB CPA State of the Trade Survey was completed by members in April so there may be an influence within the collated data.

‘Historic Sales Volumes’ for CAB Members, on balance, has doubled over the last quarter, but still fall a little behind that of the wider Construction Industry. Since growing throughout 2021, the annual ‘Historic Sales Volumes’ on balance has fallen back but still shows a healthy increase over the year to date and slightly ahead of the wider Construction Industry.

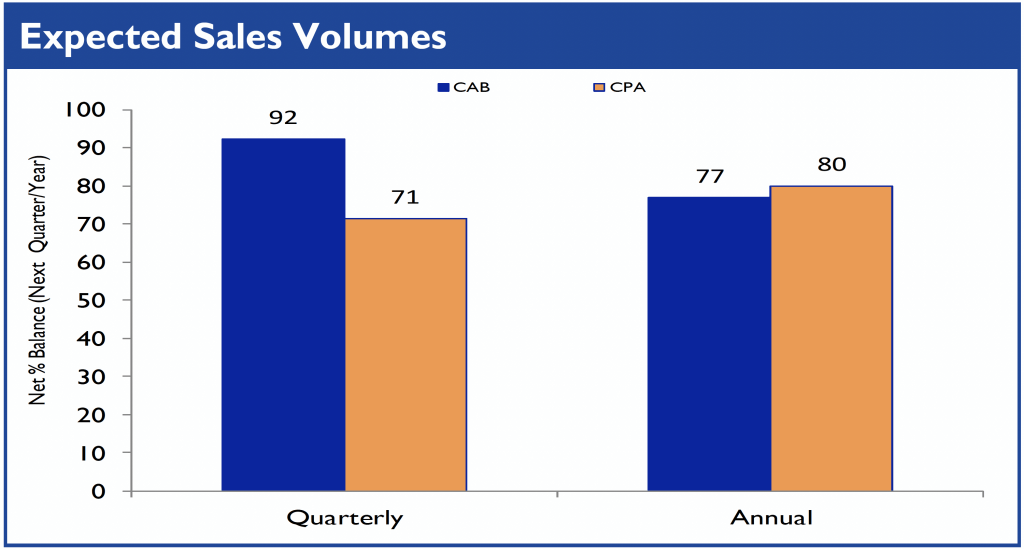

‘Expected Sales Volumes’ for CAB Members, on balance, is at its highest on a quarterly basis with 92% on net balance expecting an increase in sales in the second quarter of 2022. Whilst not at its highest over the last year, ‘Expected Sales Volumes’ for the year ahead is reported at a healthy increase of 77% on net balance of Members. This closely follows the expected growth of the wider Construction Industry.

‘Sales Volumes – Quarter-on-Quarter’ show a further slowing of growth for CAB Members in the last quarter compared to 2021. Whilst still positive, Members reporting ‘Sales Volumes’ up by over 5% have halved over the year to 46% of reporting Members. ‘Sales Volumes – Year-on-Year’ are broadly positive with only 8% of Members stating sales had decreased over the last year.

Confirmation, if any is needed, comes through clearly in the survey regarding Historic Unit Costs and Expected Unit Costs. On net balance all members of CAB and the wider Construction Industry has incurred increased costs and anticipate costs to increase further in the next quarter and the year ahead.

Breaking down the ‘Cost Factors’, whilst ‘Raw Materials’ remained at a high level during 2021, 92% of Members in quarter 1 continue to suggest further increases. The first quarter of 2022 also shows that ‘Energy Costs’ and ‘Fuel Costs’ have further risen to match that of the ‘Raw Materials’, which is closely followed by ‘Wages and Salaries’. These increases will no doubt continue to fuel increased building costs and lead to further pressure on inflation.

The ‘Likely Constraints on Activity Over the Next 12 Months’ shows an improving situation over the last year when 42% of members reported in Q2 2021 that ‘Material Supply’ would be a constraint, now falling to 23% in the last quarter. Demand remains the highest ‘Likely Constraint’ as reported by 46% of the Membership.

With ‘Historic Capacity Utilisation’, the proportion of Members who are reporting over 90% Capacity Utilisation, peaked in Q3 2021 at 44% for the previous quarter and 50% for the previous year. This has fallen over the last quarter to just 23% for both the last quarter and year. This suggests a slowing of sales output which could be attributed to both the last quarters storms and the shortage of materials. The wider Construction Industry is reporting 45% ‘Capacity Utilisation’ which would suggest new starts on site which will eventually lead through to Members sales.

Expected Capacity Utilisation by CAB Members is cautious with only 38% forecasting over 90% Capacity Utilisation for the month and year ahead. With the wider Construction Industry forward view also cautious, this could suggest a slowing in UK construction output.

‘Labour Costs’ remain at their highest level with increases over the last year and 85% of all respondents on balance claiming future increases.

Based at the picturesque Bonds’ Mill development in Stonehouse, CAB staff are always on hand during normal working hours to answer any membership, training or technical aluminium fenestration related questions. News and event information is regularly updated on the CAB website at www.c-a-b.org.uk and also in the Association monthly ezine ‘A Window Into Aluminium’ which is free to sign up to. If you are not a member of CAB and wish to learn more about membership, please contact Jessica Dean at the CAB offices by email jessica.dean@c-a-b.org.uk or telephone Jessica at the office on 01453 828851.