by Phil Slinger – CAB Chief Executive

The Construction Products Association (CPA) have reported that, on net balance, 12% of ‘heavy side’ firms saw sales fall in Q3, the first quarterly fall since the pandemic-related restrictions were introduced in 2020 Q2. The Construction Industry has seen a two year sustained growth in the sector with demand the likely constraining factor in the year ahead. On the upside, inflationary pressures showed signs of easing but remained high for fuel and energy requirements.

A fall in sales for heavy side firms would indicate a reduction in project starts and as fenestration requirements can be up to twelve months from project starts, CAB Members are still reporting strong Historic Sales, 54% on net balance, which is stronger than Members reported in Q2.

As recipients completed the State of Trade Survey in early October, forecasts will be viewed in light of Kwasi Kwarteng’s mini-budget revealed on the 23rd September.

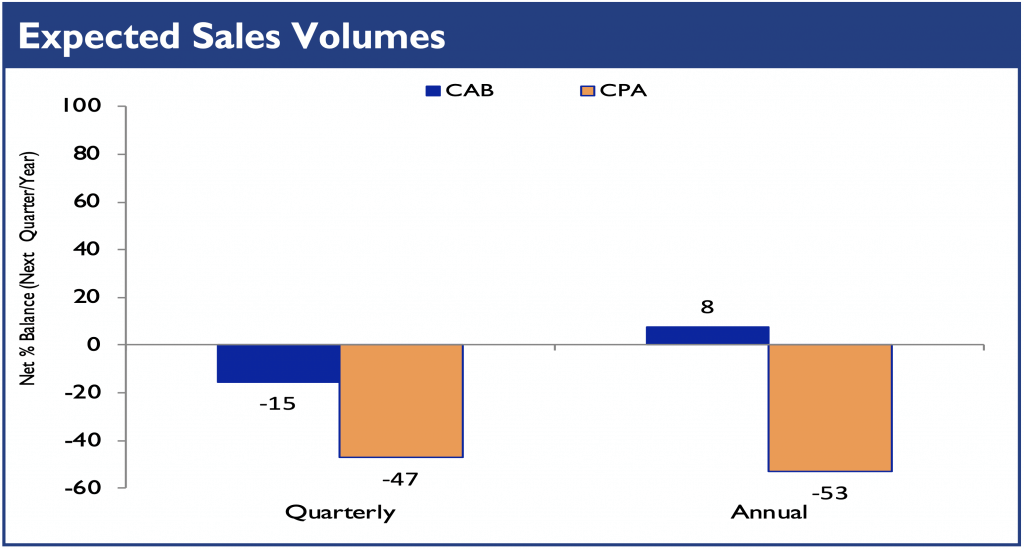

With the mini-budget in mind, looking forward the outlook is not as optimistic with 15% of Members on net balance expecting a fall in sales in the next quarter and only 8% on net balance indicating a growth in sales for the year ahead. This shows a dramatic change in outlook since Q2 where Members forecast 52% growth on net balance for the next quarter and 38% growth on net balance for the year ahead.

It would be expected that forecasts could bounce back as the UK government appears to have stabilised the financial markets with an emergency statement by the new chancellor, Jeremy Hunt on the 17th October.

Sales Volumes – Quarter-on-Quarter, the majority of Members, 54%, are reporting an increase of over 5% growth, only 15% of Members reported a reduction in sales of up to 5%. This shows a little softening over Q2 where 67% of Members reported an increase, quarter on quarter, of over 5%. Sales Volumes – Year-on-Year continue to show strong increases.

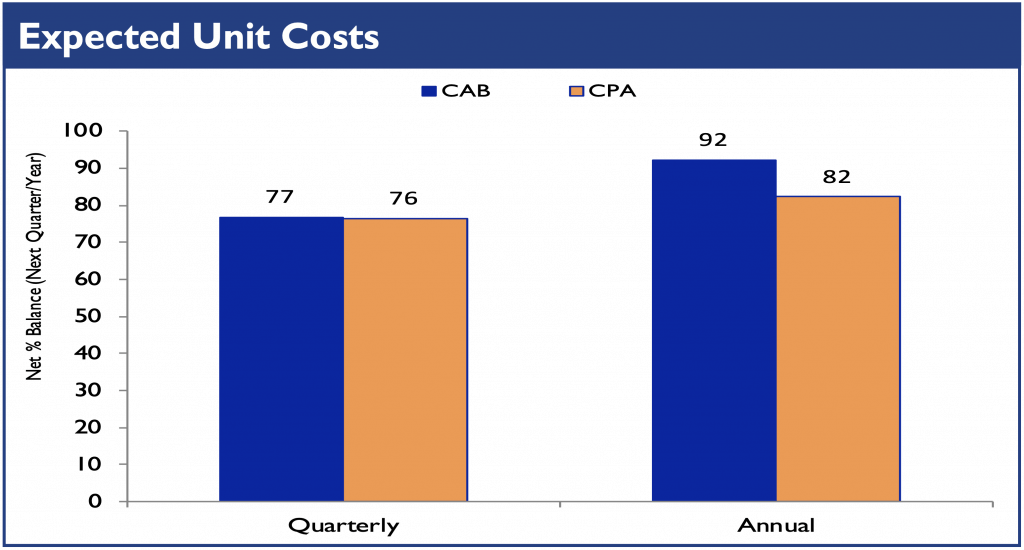

Historic Unit Costs remain high for all construction product companies, but do show a slight softening over Q2 figures. Expected Unit Costs are forecast by all companies to remain high for the next quarter and year head.

Energy costs remains the biggest influence on Cost Factors with Members reporting increases 100% on net balance. Fuel costs have softened a little since Q2 where it was reported as the biggest influence at 100% on net balance. Third most influential, Wages & Salaries has softened a little since Q2 falling back to 77% on net balance.

Likely Constraints on Activity Over the Next 12 Months reported during 2022, remains product Demand. This has increased over the year from 46% of respondents in Q1 to 77% in Q3 indicating uncertain times ahead for Members.

Historic Capacity Utilisation, members reporting operating above 90%of capacity has grown since Q1 from 23% to 54% in Q3 quarter on quarter. Expected Capacity Utilisation looking to the next quarter 38% and year 46% of members reporting operating above 90% of capacity indicates reasonable long term order books. Members Expected Capacity Utilisation is just slightly ahead of that reported by the wide Construction Industry.

The pressure on labour costs has softened slightly with a reducing number of Members on balance reporting increases, however, pressures remain and 85% of Members on balance see this as an ongoing concern. Members fears of increases in labour costs is ahead of the wider Construction Industry suggesting a lack of an available skilled labour pool.

In Q1 and Q2 Capital Investment on net balance has centralised on Product Improvement, in Q3 this has changed and now the emphasis both in the past year and year ahead, is centralised in Plant & Equipment. This could be as result of pressures on reducing costs by introducing more energy efficient machinery. This is supported by the fact that members have also increased their Capital Expenditure in property growing from 33% in Q1 and Q2 to 50% of Members on net balance in Q3.

Whilst the Q3 State of Trade Survey report offers reasonable stability in turbulent times, it remains to be seen what future budgets will be brought forward by the UK Government in order to curb a high inflation rate. No doubt these will be reflected in the next quarterly report.CAB News and event information is regularly updated on the CAB website at www.c-a-b.org.uk and in the Association’s monthly ezine ‘A Window Into Aluminium’ which is free to sign up to. If you are not a member of CAB and wish to learn more about membership, please contact Jessica Dean at the CAB offices by email jessica.dean@c-a-b.org.uk or telephone Jessica at the office on 01453 828851.